By Edidiong Udoh

The Quiet Bias in Innovation Conversations

Across global tech conversations, innovation is often equated with software.

Apps. Platforms. AI models. Fintech layers. Cloud tools.

Meanwhile, hardware: physical engineering, manufacturing, energy systems, embedded electronics, receives less attention, less funding, and significantly less narrative momentum.

This imbalance is even more pronounced across African markets.

Yet this is the paradox:

In regions where infrastructure gaps are most visible, hardware innovation may be the more foundational layer of transformation.

Not everything can be solved with an app.

Some problems require metal, circuits, fabrication, and physical systems.

Why Hardware Gets Overlooked

There are structural reasons for the bias.

1. Capital Intensity

Software scales cheaply. Hardware does not.

Hardware requires:

Prototyping materials

Fabrication tools

Testing equipment

Manufacturing runs

Logistics

The barrier to entry appears higher. Investors often perceive longer return timelines.

But this perception ignores something important:

Hardware businesses, once validated, tend to build stronger defensibility and deeper moats.

2. Infrastructure Constraints

Stable electricity, precision tools, and supply chain consistency are essential for hardware ecosystems to thrive.

Where these are inconsistent, momentum slows.

This has historically limited growth in advanced manufacturing clusters across several African economies.

Yet constraints often create the strongest innovation incentives.

Engineers working within limits design for efficiency, modularity, and resilience.

The Shift Already Underway

The undervaluation narrative is outdated.

Three observable shifts suggest hardware innovation is gaining structural momentum.

1. The Rise of Local Fabrication Labs

Across major cities, fabrication labs and maker spaces are becoming more common.

3D printing, CNC machining, laser cutting, PCB prototyping — tools once confined to advanced industrial ecosystems — are increasingly accessible.

Globally, the maker movement accelerated through institutions like the MIT Media Lab and distributed fabrication networks.

Today, that philosophy is localised: build what you need, where you need it.

Access to rapid prototyping tools reduces the time between idea and validation.

And speed matters.

2. Energy Innovation as Hardware Catalyst

Energy constraints have unintentionally accelerated hardware creativity.

Solar inverters are being assembled locally. Battery management systems are being customised for local climate realities. Hybrid systems are being engineered to bridge grid instability.

Hardware becomes practical when it solves immediate pain points.

In markets where power reliability is inconsistent, energy hardware is not experimental; it is essential infrastructure.

3. Global Supply Chain Reconfiguration

Post-pandemic supply chain disruptions forced companies worldwide to rethink over-centralised manufacturing models.

Distributed production and regional assembly are increasingly strategic priorities.

This creates opportunity.

Regions that develop lightweight, modular manufacturing capabilities can integrate into global value chains more effectively than before.

Hardware innovation is no longer purely about heavy industry.

It is about smart, modular, adaptive production.

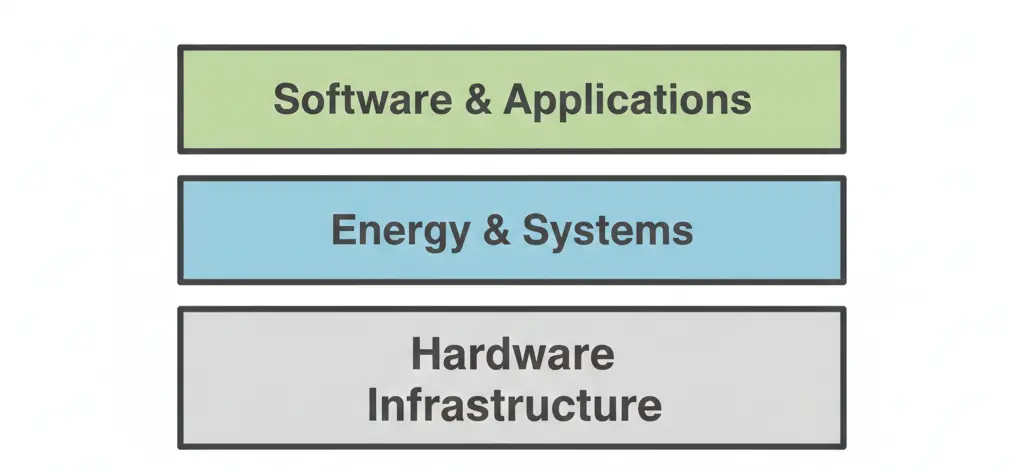

The Software Ceiling Problem

Software ecosystems grow fastest when built on stable hardware foundations.

Fintech requires reliable mobile devices and network infrastructure.

E-commerce requires logistics systems.

AI requires compute infrastructure and power stability.

Without physical systems, digital growth plateaus.

This is the ceiling problem.

And it explains why hardware innovation may become the next multiplier.

Why the Next Decade Will Look Different

Several trends suggest that hardware’s profile will rise significantly:

Declining cost of rapid prototyping tools

Growth of engineering-focused education pathways

Increased cross-border technical collaboration

More founders combining software + hardware solutions

Climate and energy pressures are demanding physical systems

The hybrid founder, comfortable with firmware, fabrication, and frontend, may define the next wave.

Not purely a coder. Not purely an engineer. But both.

What Builders Should Focus On

For innovators considering hardware:

Design modularly.

Reduce component dependency where possible.

Build for maintainability, not just launch.

Validate with real-world use cases early.

Document thoroughly — reproducibility increases trust.

The goal is not to replicate industrial giants overnight.

The goal is to solve immediate, high-friction problems with engineered solutions.

The Strategic Opportunity

Narratives shape investment.

When hardware is framed as expensive and risky, it receives less attention.

When it is reframed as foundational and defensible, it attracts builders.

In many African markets, the next transformative companies may not begin as apps.

They may begin as engineered systems solving physical constraints.

Energy devices. Agricultural machinery. Modular manufacturing units. Embedded systems.

The shift will not be loud at first.

But it will be structural.

The Strategic Opportunity

Narratives shape investment.

When hardware is framed as expensive and risky, it receives less attention.

When it is reframed as foundational and defensible, it attracts builders.

In many African markets, the next transformative companies may not begin as apps.

They may begin as engineered systems solving physical constraints.

Energy devices. Agricultural machinery. Modular manufacturing units. Embedded systems.

The shift will not be loud at first.

But it will be structural.

Final Thought

Innovation conversations need recalibration.

Software is powerful, but without hardware, software floats and the builders who understand both layers, who can translate local challenges into engineered solutions, may define the next phase of growth.Hardware is not behind. It is simply under-credited. That is changing.

1. The Rise of Local Fabrication Labs

3. Global Supply Chain Reconfiguration